Categories

Homeowner Education, Mortgage & Financing Education, Real Estate EducationPublished January 14, 2026

What Would a 50-Year Mortgage Actually Look Like?

What Would a 50-Year Mortgage Actually Look Like?

There’s been growing conversation around the idea of introducing 50-year mortgages. Before reacting emotionally, it helps to step back and look at the math and the intent behind longer loan terms.

This post breaks down what these loans actually look like in practice, using real numbers and side-by-side comparisons so you can see how payments, equity, and total cost change over time.

🔍 Quick Summary

Same house. Same loan amount. Very different outcomes.

- 15-year mortgages build equity the fastest

- 30-year mortgages balance payment and ownership

- 40- and 50-year mortgages lower early payments but slow equity growth

- Most homeowners sell in 5–10 years, which changes how these loans actually perform

Baseline Assumptions (Used in Every Example)

To keep everything apples to apples, every example below uses the same purchase structure:

- 🏡 Purchase price: $625,000

- 💰 Down payment: $125,000 (20%)

- 📄 Loan amount: $500,000

- 📉 PMI, taxes, insurance, HOA: Not included

- 📊 All figures reflect principal & interest only

These exclusions are intentional. Property taxes, insurance, and HOA dues vary widely and would muddy the comparison. This post focuses strictly on how loan terms and interest affect payments and ownership.

💡 A Quick Note on 40-Year Mortgages

40-year mortgages are not new. They’ve existed in various forms since the early 2000s and became more visible after the 2008 housing crisis.

Today, they are most commonly offered as:

- Loan modifications, or

- Specialty non-QM products

They are not widely used for traditional home purchases, which is important context when discussing why lenders are now floating the idea of 50-year terms.

The goal is not to replace 30-year mortgages. The goal is to reduce monthly payment pressure for affordability-constrained buyers.

Example 1: Standard 30-Year Fixed Mortgage

Loan Details

- Loan amount: $500,000

- Interest rate: 6.5%

- Loan term: 30 years

First Monthly Payment Breakdown

- Total principal & interest: $3,160

- Interest: $2,708

- Principal: $452

Early in a 30-year loan, most of your payment goes toward interest. The shift toward principal happens slowly.

When the Principal Finally Overtakes Interest

- Month 233 (just over 19 years in)

At that point, you are finally paying more toward ownership than borrowing.

Total Cost Over 30 Years

- Total interest paid: $637,722

- Total paid: $1,137,722

That’s nearly double the original purchase price.

What This Looks Like in Real Life

Most homeowners don’t stay for 30 years.

If you sold after 7 years:

- Principal paid: $47,918

- The majority of payments still went toward interest

Example 2: 15-Year Fixed Mortgage

Loan Details

- Loan amount: $500,000

- Interest rate: 5.35%

- Loan term: 15 years

First Monthly Payment Breakdown

- Total principal & interest: $4,052

- Interest: $2,239

- Principal: $1,822

Right out of the gate, a much larger portion of your payment goes toward ownership.

When Principal Overtakes Interest

- Month 26 (just over 2 years in)

Total Cost Over 15 Years

- Total interest paid: $229,418

- Total paid: $729,418

Sold After 7 Years?

- Principal paid: $184,378

That’s nearly four times more equity than the 30-year loan over the same timeframe.

Example 3: 40-Year Mortgage With Interest-Only Period

Loan Details

- Loan term: 40 years

- Interest rate: 7.125%

- Interest-only period: 10 years

First 10 Years

- Monthly payment: $2,969

- Principal paid: $0

- Remaining balance: $500,000

Despite making consistent payments, the loan balance does not decrease.

After the Interest-Only Period

- Principal payments begin

- Monthly payment increases to approximately $3,369

When the Principal Finally Overtakes Interest

- Month 247 (20+ years in)

Total Cost Over 40 Years

- Total paid: $1,568,973

⚠️ Real-World Impact

If you sold anytime in the first 10 years: You would still owe the full $500,000

Example 4: What a 50-Year Mortgage Would Likely Look Like (Speculative)

This example is educational only. As of today, 50-year mortgages are not standard consumer loans.

Assumed Loan Structure

- Loan term: 50 years

- Estimated interest rate: 7.5%

- Interest-only period: 20 years

First 20 Years

- Monthly payment: $3,125

- Principal paid: $0

- Total interest paid: $750,000

After the Interest-Only Period

- Monthly payment increases to approximately $3,496

When the Principal Finally Overtakes Interest

- Month 490 (around 41 years in)

Total Cost Over 50 Years

- Total paid: $2,008,586

Sold After 7 Years?

Principal paid: $0

What Would a 50-Year Mortgage Actually Look Like Visualized?

Same house. Same loan. Very different outcomes.

Baseline Assumptions (Applies to Every Example)

🏡 Purchase price: $625,000

💰 Down payment: $125,000 (20%)

📄 Loan amount: $500,000

📉 PMI, taxes, insurance, HOA: Not included

📊 All numbers reflect principal & interest only

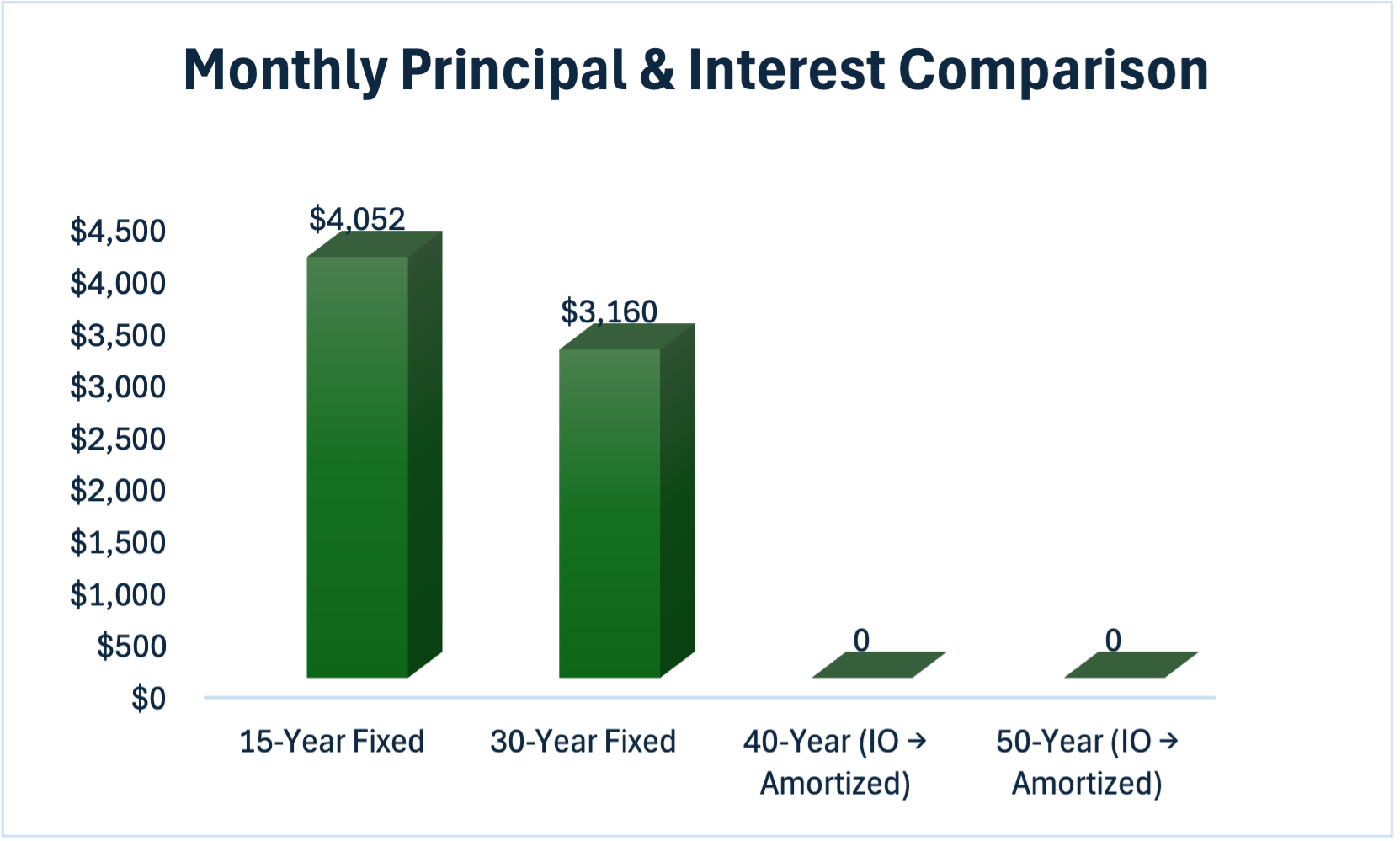

Side-by-Side Mortgage Comparison |

||||||

| Loan Type | Rate | Term | Monthly P&I | Interest Paid (Full Term) | Total Paid | Principal After 7 Years |

| 15-Year Fixed | 5.35% | 15 yrs | $4,052 | $229,418 | $729,418 | $184,378 |

| 30-Year Fixed | 6.50% | 30 yrs | $3,160 | $637,722 | $1,137,722 | $47,918 |

| 40-Year (IO → Amortized) | 7.13% | 40 yrs |

$2,969 (yrs 1–10) to $3,368 (after IO) |

$1,068,973 | $1,568,973 | $0 |

| 50-Year (IO → Amortized) | 7.50% | 50 yrs |

$3,125 (yrs 1–20) to $3,496 (after IO) |

$1,508,586 | $2,008,586 | $0 |

When Do You Start Paying More Principal Than Interest? |

||

| Loan Type | Month | Years In |

| 15-Year Fixed | Month 26 | ~2 years |

| 30-Year Fixed | Month 233 | ~19 years |

| 40-Year (IO → Amortized) | Month 247 | ~20+ years |

| 50-Year (IO → Amortized) | Month 490 | ~41 years |

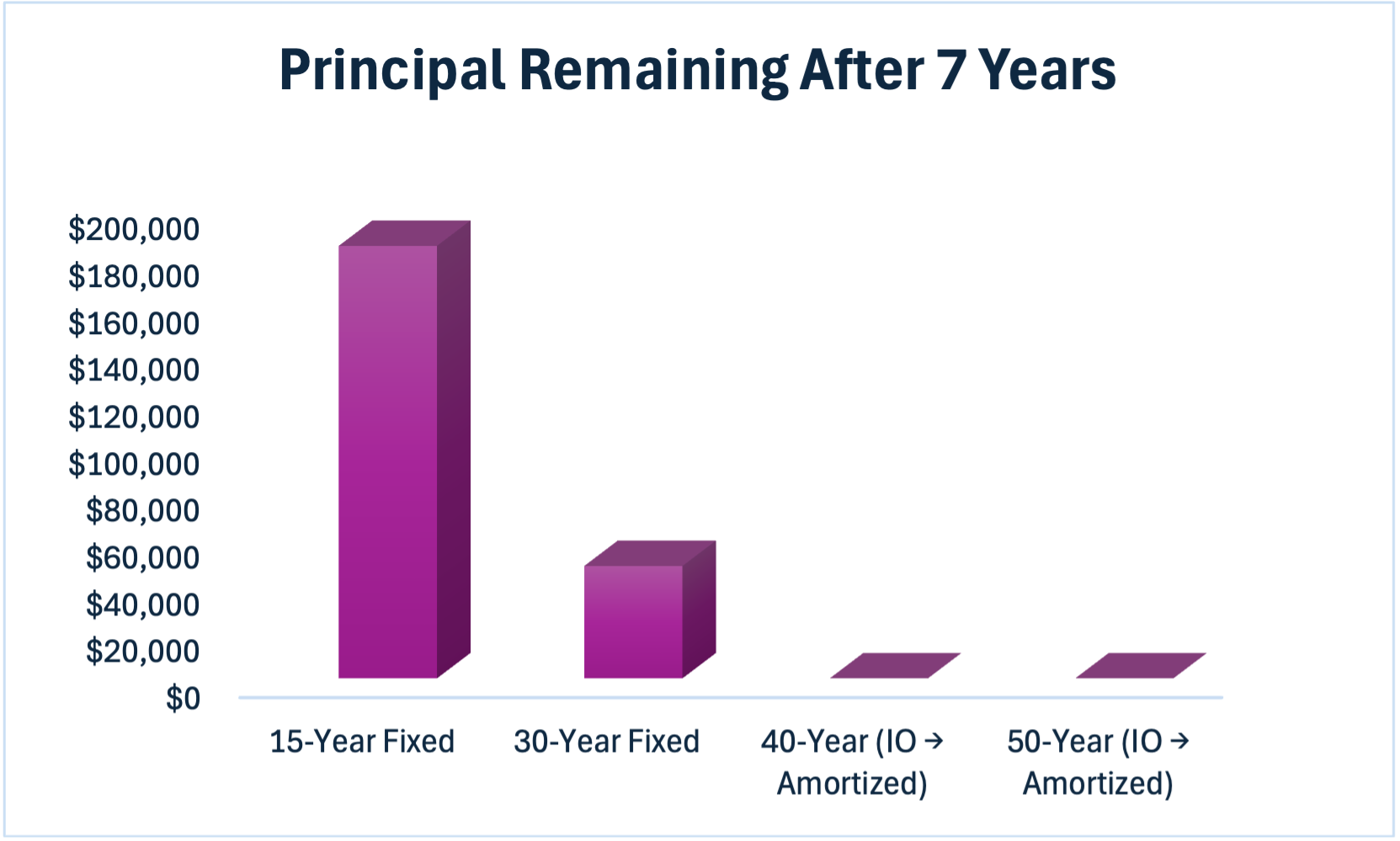

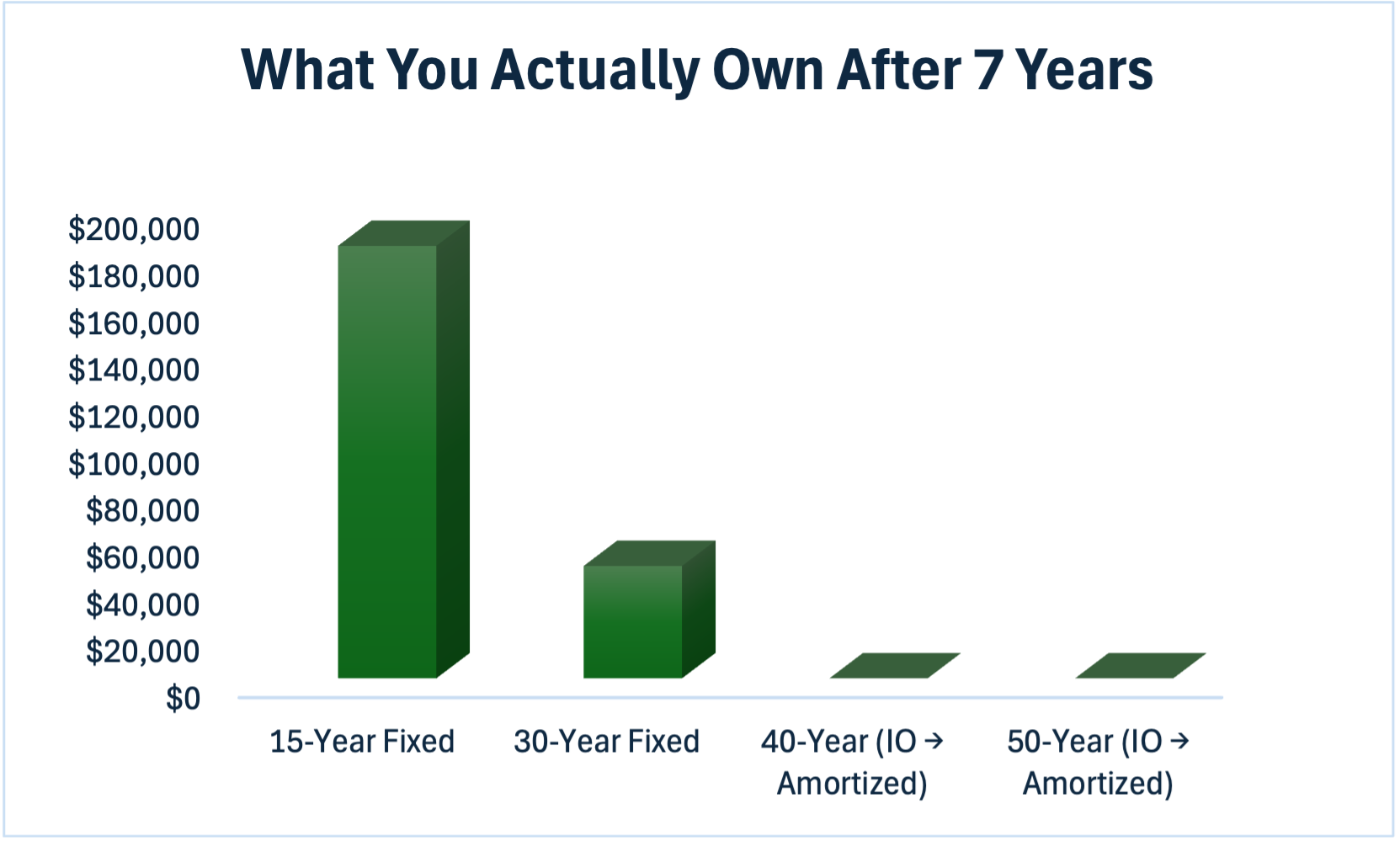

What You Actually Own After 7 Years |

|

| 15-Year Fixed | $184,378 |

| 30-Year Fixed | $47,918 |

| 40-Year (IO → Amortized) | $0 |

| 50-Year (IO → Amortized) | $0 |

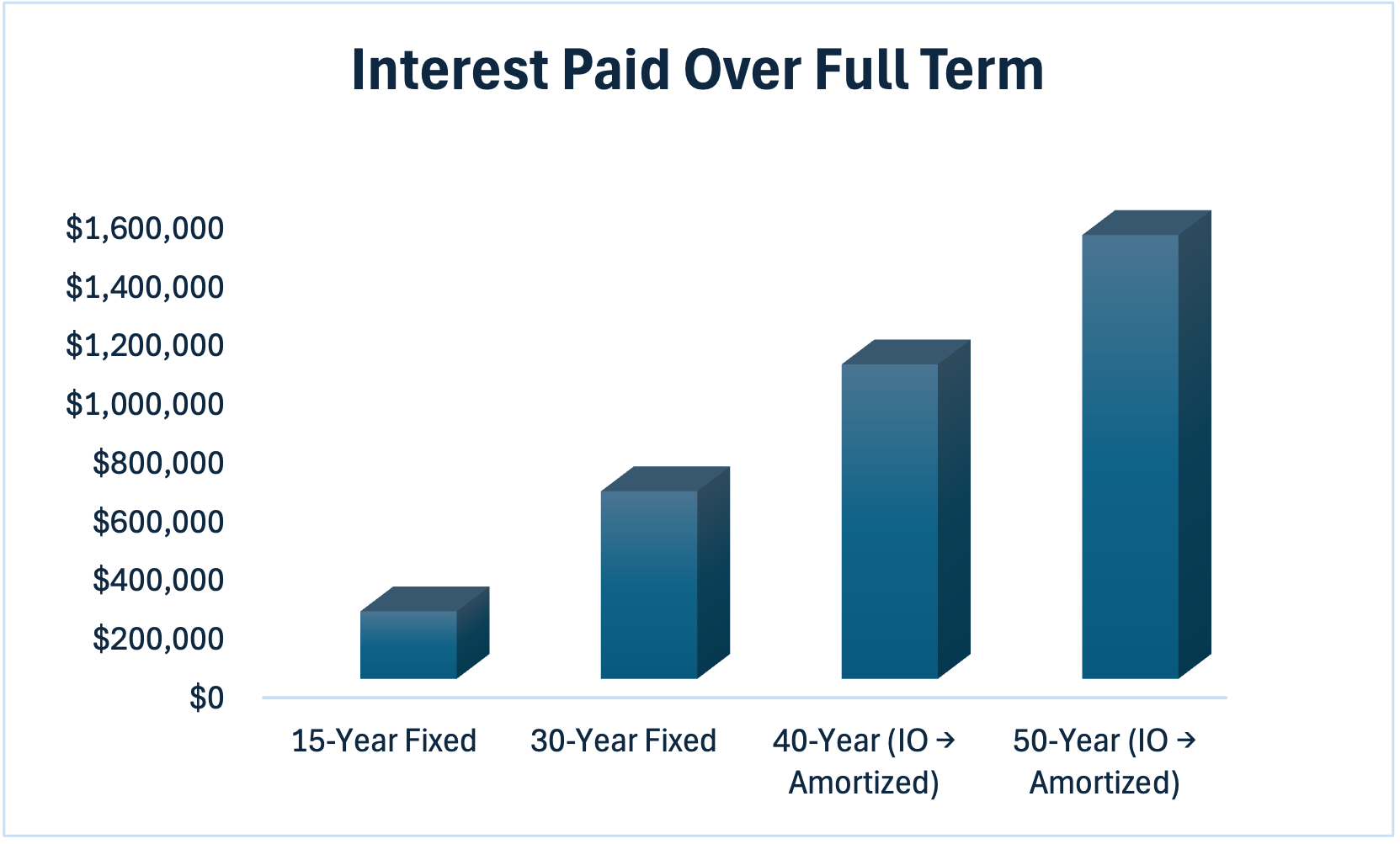

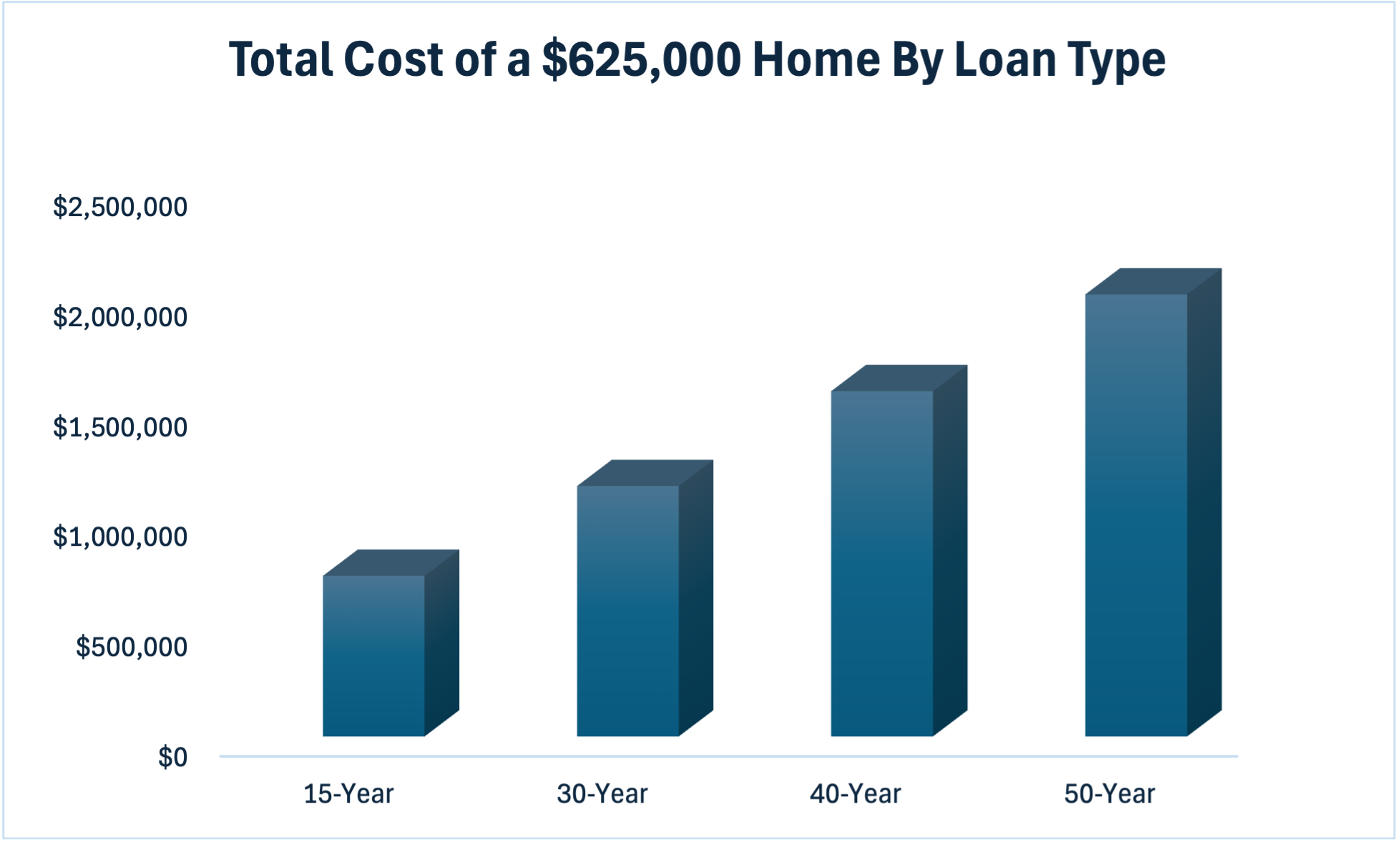

Total Cost of a $625,000 Home |

|

| Loan Term | Total Paid |

| 15-Year | $729,418 |

| 30-Year | $1,137,722 |

| 40-Year | $1,568,973 |

| 50-Year | $2,008,586 |

Key Takeaway

Longer loan terms improve monthly affordability, not ownership speed.

Who Longer Loan Terms Might Make Sense For

- Buyers prioritizing monthly cash flow

- Buyers with fluctuating income

- High-income buyers planning large future principal paydowns

Who Longer Loan Terms Likely Do Not Make Sense For

- Buyers focused on building equity through principal payoff

- Anyone assuming lower payments mean a cheaper home

- Buyers stretching their budget just to qualify

- Anyone relying on refinancing as a guarantee

⚠️ A Reality Check on Refinancing

Refinancing depends on:

- Lower interest rates

- Stable income

- Strong credit

- Favorable appraisal

- Any one of these changes can derail that plan.

Final Takeaway

Longer mortgage terms are about affordability, not faster payoff.

The right mortgage isn’t the shortest or the longest term.

It’s the one that aligns with:

- How long you realistically plan to own the home

- Your cash-flow priorities

- Your tolerance for risk

Running the numbers upfront matters more than the headline payment.

|

or another way